It’s a scenario no one wants to think about. A married couple goes on holiday, and a sudden accident means they both pass away at the same time. Beyond the emotional shock for their families, a difficult legal question arises: What happens to their home, savings, and assets? When it’s impossible to tell who died first, who inherits what?

This is where things can become complicated, and the law must intervene. The outcome often depends on one very important document, specifically a provision in a will that addresses simultaneous death.

What Does the Law Say About Simultaneous Death?

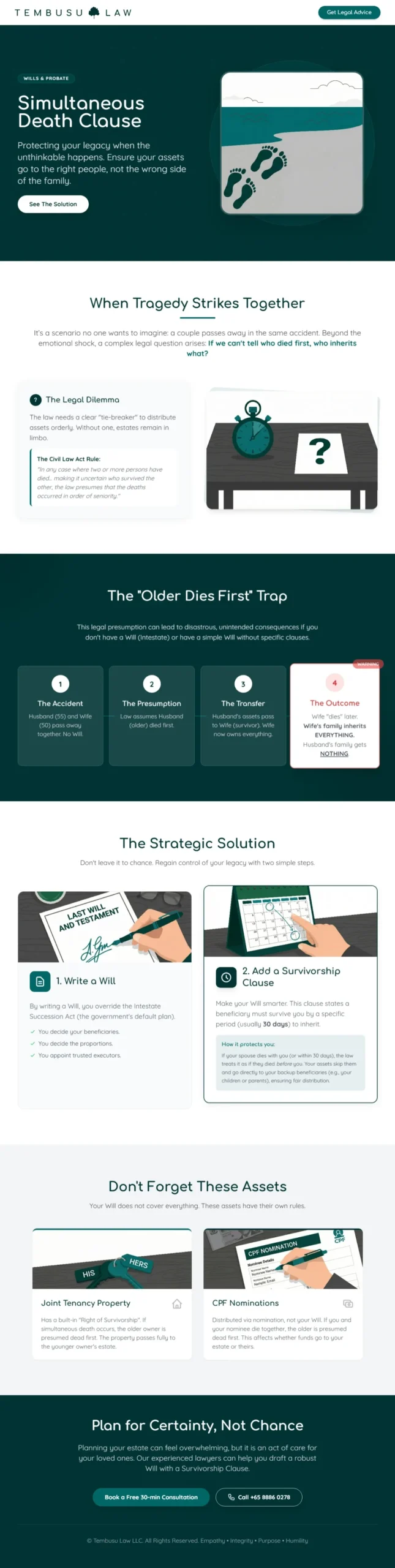

This scenario is unsettling for many people. When family members pass away together, and it’s genuinely impossible to tell who died even a moment before the other, how does the law cope?

The law needs a clear “tie-breaker” to prevent a legal gridlock. If it cannot be determined who survived whom, the estates would be left in limbo.

To solve this, the law has a specific rule, which is found in the Civil Law Act. This rule states:

In any case where two or more persons have died in circumstances making it uncertain who survived the other, the law presumes that the deaths occurred in order of seniority.

What does this mean in plain English? The older person is legally presumed to have died first. The younger person is deemed, for all legal and inheritance purposes, to have survived the older one.

This may sound unusual, but it is a practical solution. It is not about what actually happened; it is a legal tool used to facilitate the orderly distribution of assets. This simple rule, however, can have massive and often unwanted consequences, which is why planning is so important.

Why Is This Legal Presumption a Problem?

Let’s imagine a husband and wife die in the same incident, and they do not have Wills. This means their assets will be distributed according to the Intestate Succession Act.

Now, let’s apply the legal rule.

- Scenario: The husband is 55, and the wife is 50. They have no children.

- Step 1: Because the husband is older, the law presumes he died first. Under the intestacy rules, his assets (including his share of any joint assets) would pass to his surviving spouse, the wife.

- Step 2: The wife, presumed to have died moments later, now owns her original assets plus all of her husband’s assets.

- Step 3: Since the wife also died without a Will, her now-enlarged estate passes to her family (for example, her parents or siblings).

- The Result: The husband’s family gets nothing. This is almost certainly not what the couple would have wanted.

How a Will Solves This (And How to Make It Even Better)

Relying on that default “older dies first” rule can lead to disaster. Let’s explore how you can regain control.

The First Solution: Having a Will

Firstly, having a valid Will is a significant step. A Will is your personal instruction manual for your assets. When you die without one, your estate is distributed according to a fixed, one-size-fits-all formula set by the government (the Intestate Succession Act).

This is where the “older dies first” rule can cause the most problems, like a husband’s entire family being accidentally disinherited.

By writing a Will, you override the Intestate Succession Act.

You get to decide:

- Who gets your assets (your beneficiaries)?

- How much do they get?

- Who is in charge of managing the process (your executor)?

This means that instead of the law guessing, you have left clear instructions. This solves the first big problem.

The Better Solution: Adding a Survivorship Clause

Now, let’s make your Will even smarter. A simple Will might say, “I leave everything to my spouse.” But what happens in a simultaneous death?

The “older dies first” rule could still apply. The older spouse’s assets would pass to the younger spouse (as per their Will), and then all the combined assets would pass to the beneficiaries named in the younger spouse’s Will. This might still not be what you wanted.

The best solution is to include a specific clause, often called a simultaneous death clause or, more commonly, a “survivorship clause”.

This clause is a simple but powerful instruction. It says that for any beneficiary to inherit from your Will, they must survive you by a specific period, usually 30 days.

Here is how it works:

- A couple, both with this 30-day clause in their Wills, pass away in the same incident.

- When the executor looks at the husband’s Will, they must ask: “Did the wife survive him by 30 days?” The answer is no.

- Because she did not, the law, for the purposes of the will’s simultaneous death clause, treats her as if she had passed away before him.

- Therefore, the inheritance does not go to her estate. Instead, it “skips” her and goes directly to the husband’s next choice of beneficiaries (his contingent beneficiaries), perhaps his children or his siblings.

- Exactly the same thing happens with the wife’s Will. The husband did not survive her by 30 days, so her assets go directly to her chosen contingent beneficiaries.

This simple clause is the most effective way to prevent your assets from being accidentally passed to the wrong people. It ensures your legacy is protected and your wishes are followed, no matter what.

What About Assets Outside Your Will?

It’s important to remember that not all your assets are covered by your Will.

How Are Joint Tenancy Properties Handled?

Many couples own their homes as “joint tenants.” This means the property has a “right of survivorship” built in. If one owner dies, the property automatically passes to the surviving owner, regardless of what the Will says.

In a simultaneous death, the legal presumption (that the older person dies first) applies. The property would pass to the younger co-owner and then become part of their estate. This is another situation where your intentions can be defeated without careful planning.

What Happens to CPF Nominations?

Your CPF savings are also separate from your Will. They are distributed based on the nomination you make with the CPF Board.

If you and your nominee (for example, your spouse) die at the same time, the CPF Board also follows the rule: the older person is deemed to have died first.

If the older spouse nominated the younger, the CPF savings will be paid to the younger spouse’s estate. If the younger spouse’s nominee (the older spouse) is already presumed dead, their CPF savings may be distributed to their estate. This can get complicated and may not be what you wanted.

Conclusion About the Simultaneous Death Clause in Your Will

Reflecting on these situations is challenging, but planning for them is an act of care for the loved ones you leave behind. Relying on legal presumptions can lead to unintended and unfair outcomes, which can cause confusion and distress for your family.

A well-drafted Will, which includes a survivorship clause, gives you control. It ensures your assets are distributed according to your true wishes.

Planning your estate can feel overwhelming, but you don’t have to do it alone. For clear and compassionate advice, get in touch with the best family and Divorce lawyers in Singapore at Tembusu Law.

Contact us today for a free 10-minute discovery call.

Frequently Asked Questions About the Simultaneous Death Clause in Your Will

What Is the Main Law for Simultaneous Death in Singapore?

The main legal rule is in the Civil Law Act. It states that if two or more persons die in circumstances where it is uncertain who died first, the deaths are presumed to have occurred in order of seniority. This means the older person is legally considered to have died first.

What Happens if a Married Couple Dies Together Without a Will?

Their assets will be distributed according to the Intestate Succession Act, combined with the presumption that the older spouse died first. This often results in the entire combined estate passing to the family of the younger spouse, while the older spouse’s family receives nothing.

Does a Will Automatically Protect Me from This Problem?

A Will is essential, but a simple Will might not be enough. If you leave everything to your spouse, the legal presumption could still apply. A Will with a “survivorship clause” (or simultaneous death clause) is the best way to ensure your assets are distributed to your intended contingent beneficiaries.

How Long Is a Typical Survivorship Period in a Will?

A typical survivorship period is 30 days. This is generally long enough to avoid the problems of a simultaneous death scenario while not delaying the estate’s administration unnecessarily.

Are My CPF Savings and My House Covered by My Will?

Not always. Your CPF savings are distributed according to your CPF nomination, not your Will. A house owned under “joint tenancy” automatically passes to the surviving joint owner. Both of these can be affected by the simultaneous death presumption, so they require separate and careful planning.